This article can be found on the EnergyLogic website here

A Closer Look at Delinquencies & Foreclosures

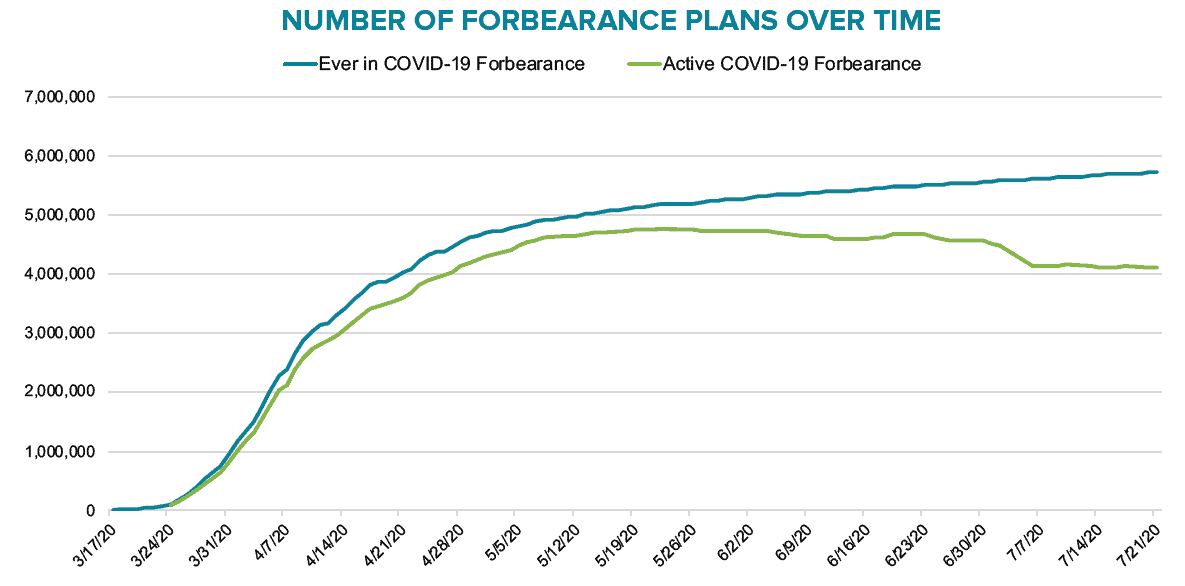

In his recent blog, “Where Are the For Sale Signs,” Housing Tides’ Jeff Whiton proposed that the present shortage of housing inventory will end if government foreclosure protections are not extended. Housing finance firm Black Knight estimates that as of July 21, 4.1 million homeowners continue to receive mortgage forbearance benefits from their lenders, making up 7.8% of U.S. mortgages. 1.87 million of these homeowners are “seriously delinquent,” or 90+ days late on their payments.

Black Knight’s Mortgage Monitor report shows 4.1 million mortgages in forbearance as of July 21.

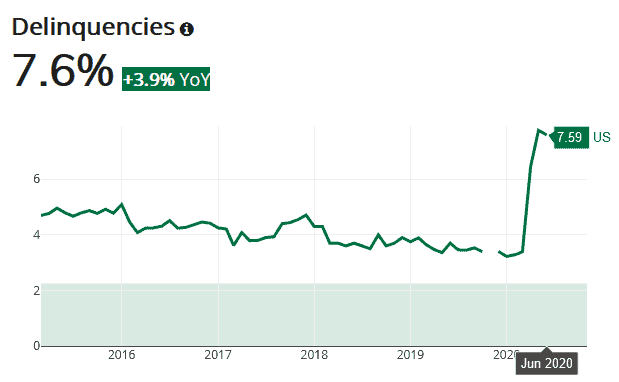

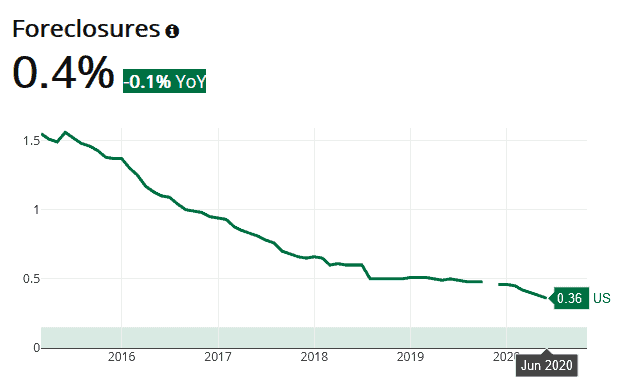

Black Knight data show since 2005 the average ratio of seriously delinquent mortgages to those in foreclosure was 1.4. Foreclosure protections for government-backed mortgages have thus far prevented a widespread foreclosure crisis, and the ratio of seriously delinquent borrowers to active foreclosures has risen sharply, reaching 9.75 as of June 30.

Total delinquencies vs active foreclosures data shown in Housing Tides.

Total delinquencies vs active foreclosures data shown in Housing Tides.

What's the Worst That Could Happen?

Even with states like Florida and Pennsylvania extending protections, they’re slated to end on August 31. Without additional government intervention, a reversion to the mean suggests that the number of foreclosures could rise to 1.34 million (1.87M seriously delinquent / 1.4 = 1.34M foreclosures). Redfin data show just 1.16 million homes listed for sale in the U.S. in June. The foreclosure process takes some time to play out, especially in states where foreclosures must go through the court system, but if even a portion of these potential foreclosures happen, we’d see a meaningful increase in housing supply.

Moreover, the Washington Post’s Andrew Van Dam explains “If delinquencies lead to foreclosures, as the forbearance time period expires, we could see an increase in the number of properties on the market. It may be compounded by other stressed buyers, who need to cash out of their home to pay bills as the recession continues. The supply glut could increase further if shutdowns are lifted and homeowners who held off on selling during a pandemic suddenly flood the market.”

Eviction Protection Takes the Place of Mortgage Forbearance

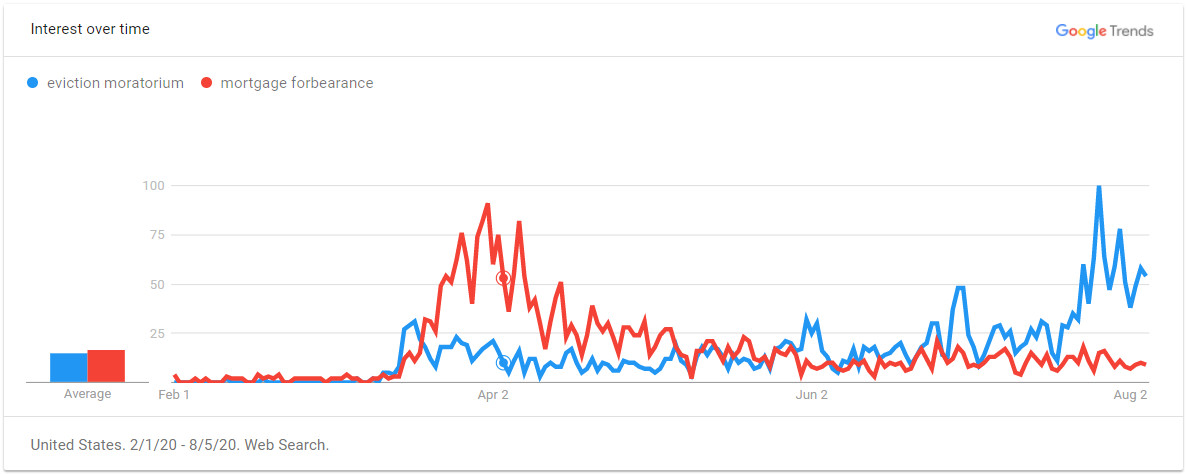

Google Trends data show that early in the pandemic, searches for “mortgage forbearance” were triple that of searches for “eviction moratorium.” This has flipped, with the latter now representing a larger share of Google searches. This suggests that financially-strapped homeowners first relied on forbearance programs to stay in their homes, but are increasingly looking to eviction prohibitions as lenders phase out forbearance aid.

Google Trends shows a recent rise in searches for “eviction moratorium”.

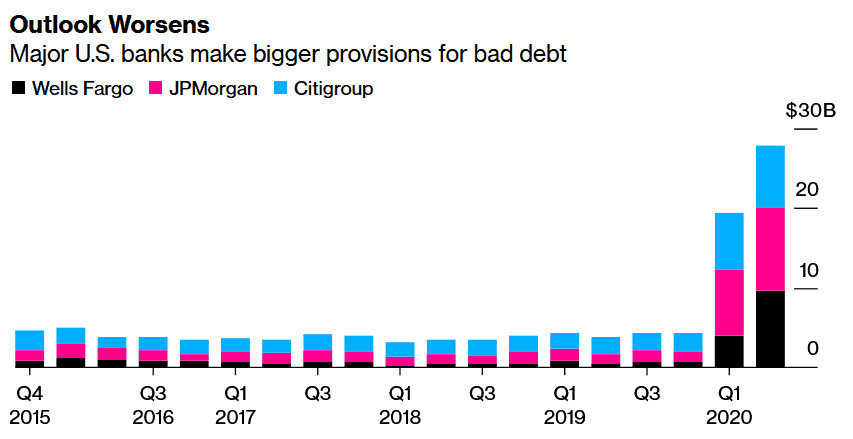

Banks Are Preparing for the Worst

Major U.S. banks see the writing on the wall. Loan loss provisions by JPMorgan, Citigroup and Wells Fargo totaled nearly $28 billion in Q2, just shy of what these banks set aside for bad debts in late 2008.

Bloomberg visualization of loan loss provisions detailed in company financial filings.

Strong Housing Demand May Weaken

Jonathan Miller writes in his July 3 Housing Notes blog that “It is important to note that the housing market was basically closed from mid-March to the last week of June. The market is just awakening and may feel like a boom, but it’s really a release of pent-up demand from the spring market that never was… Any housing market, when artificially closed during the traditionally busiest times of the month, will see a surge when it re-opens. Once the excess demand is satiated over the next month or two, then we get to see the underlying market.”

What to Look for in Coming Months

The extra federal unemployment benefits expired at the end of July. Congress is presently debating what policy measures should follow, but it’s not clear when those benefits will reach Americans that remain out of work. Most importantly, the dramatic rise in mortgage delinquencies has occurred with those extra unemployment benefits in place. The loss of $600 of income per week means that we should expect more homeowners and renters to endure financial hardship in coming months.

Access Housing Market Data in Seconds

Monitor delinquency, foreclosure and unemployment trends along with downstream effects on housing supply and home prices with Housing Tides in order to stay current on market conditions. Dive into Housing Tides' interactive interface to learn more!